China 2030

Green Transition Powerhouse for the Decade Ahead

China’s New Five Year Plan

With the publication of the 15th Five Year Plan for the economy and society, at the beginning of March Beijing set out its priorities for technological innovation, economic security, public well-being and carbon reduction in keeping with the existing major target of attaining a doubling of per capita GDP from 2020 levels by 2035.

In line with the government’s pledge to see carbon emissions peak by 2030 – a key step towards its 2060 carbon neutrality target, the country plans to slash carbon emissions per unit of GDP by a total of 17 per cent over the next five years. This year’s reduction target has been set at 3.8 per cent, following a 5.1 per cent reduction last year.

UK-China Energy Pact Highlight of Trade and Diplomatic Talks

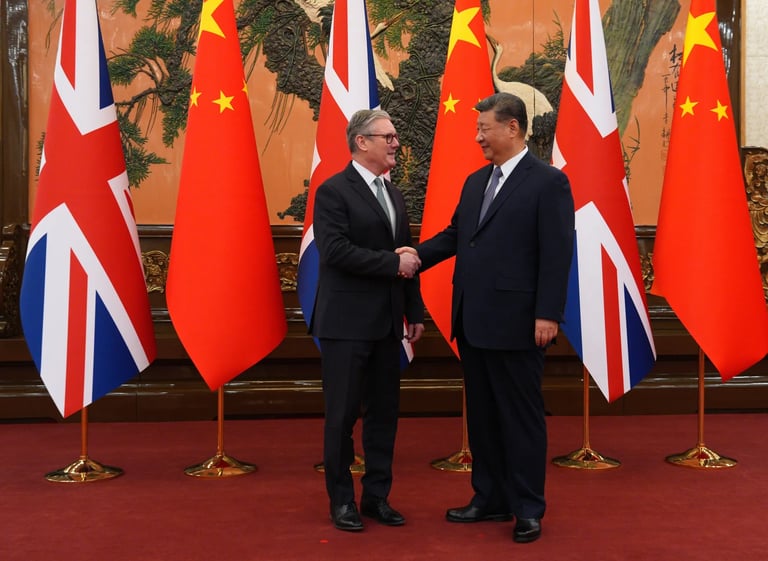

A key event at the beginning of 2026 was the UK Prime Minister Sir Keir Starmer’s diplomatic and trade visit to China — accompanied by business leaders from over 60 UK companies. One hugely prominent deal which was struck was Octopus Energy’s new joint venture with China’s PCG Power. PCG Power is a leading investment management and operation service provider for next-generation power systems. The partnership, to be named Bitong Energy, will allow Octopus to trade renewable electricity in China’s rapidly expanding clean-energy market, using its advanced energy trading software combined with PCG’s local market expertise.

The chief executive of Octopus Energy’s power generation arm, Zoisa North-Bond, commented after the announcement of the deal that the greater level of competition which the deal should stimulate could cut wind farm development costs by almost a third. If accurate, this would help the UK government meet its goal of lowering energy bills for industry and private householders. The company said that by in September it wants to deploy wind turbines from one of China’s largest manufacturers into its own projects in Britain.

A leading attraction for the UK is the Chinese firm’s high level innovation and technological expertise which could boost the UK’s renewable energy sector. The Bitong Energy venture aims to trade up to 140 terawatt-hours of renewable power annually by 2030 — which is roughly equivalent to the UK’s entire current green energy output — and is projected to generate significant profits, with an estimated valuation in excess of £500 million within five years and approximately half of annual earnings flowing back to the UK.

From the UK side Octopus can deploy state-of the-art trading techniques using its advanced energy-trading algorithms and AI platforms that can predict demand and supply; optimise renewable output (e.g. for wind, solar); and Decide when and how power should be bought or sold in local markets

Emissions Targets present challenges

China’s official goal of peak CO2 emissions by 2030 (versus the EU’s 55% reductions) and complete carbon neutrality by 2060 (versus the EU’s 2050) is seen as ambitious but not unattainable if current growth targets and industrial modalities can be maintained.

In recent years the traded price of carbon emissions in China has remained at a fraction of the EU ETS price, fluctuating at roughly between a quarter and a sixth of the EU compliance regime's price of carbon. As the strain imposed on European industry in the face of cheaper competition persisted, the EU finally adopted plans for a controversial carbon 'border tax', to be implemented in January 2026. (see Events)

Despite this notable departure from accepted norms the Chinese ETS is nevertheless the largest sytem of its kind in the world. Ambitious in its scope and potentially comprehensive in its coverage, if all the key sectors earmarked for inclusion do finally get brought into the system on a true 'cap and trade' basis. In August 2025 Beijing announced a plan to end the 'intensity' approach to controls, with phase out to begin in 2027.

The EU-Emissions Trading Scheme

Each year the EU systematically reduces allocation of EUAs, he supplies of European Union Allowances with the intent of driving up the prices of carbon emission. This strategy bolsters the Commission's commitment to fostering a market environment that encourages sustainable practices and emission reduction strategies. It illustrates Europe's continued support in the market, a remarkable commitment given the context of a land war at the door or Europe, an energy crisis, and sustained inflation.

The EU-ETS carbon pricing mechanism is designed to regulate and reduce greenhouse gas emissions. And it works, at least within its local marketplace. Over the past two decades, it has evolved into a working tool to reduce emissions at scale, operating within an increasingly well-informed and liquid market.

The EU Commission has outlined clear environmental goals for 2030 and 2050. Those include a 55% reduction in greenhouse gas emissions from 1990 levels by 2030. Also, it aims for climate neutrality by 2050 - the amount of greenhouse gasses emitted should be minimized, and any tonne of CO2 emitted should be removed or offset. To achieve these climate objectives, carbon prices are going to have to continue to increase. It is only when faced with high emission prices that industries have a clear incentive to lower emissions.

GERMANY FACES BITTER REALITY IN TRADE OFF BETWEEN GREEN GOALS AND ECONOMIC SURVIVAL

Long held up as a model of energy transition, Germany now faces the serious consequences of its nuclear phase-out. Dramatic cost increases, a weakened industrial base, increased dependence on energy imports, and strategic vulnerability: the choices made in the name of anti-nuclear ideology have profoundly destabilized the German energy system. Friedrich Merz now acknowledges the country’s strategic error, but the challenge now goes far beyond recognizing the situation: There is very little remaining room for manoeuver to correct a course set more than twenty years ago, largely by the iconic Angela Merkel and her contemporaries, who gladly accepted dependence on Russian gas in exchange for a lower national energy bill.

Today, in a context of growing electricity demand and persistent geopolitical tensions, this strategy’s weaknesses have been laid bare. Energy is more than ever the lifeblood of the economy: without energy, everything collapses. Yet, for the past twenty to twenty-five years, Germany has believed it could do without non-renewable energy sources and that only wind power—and to a lesser extent solar power, was acceptable. This wind power monoculture went hand-in-hand with a non-growth ideology championed by German environmentalists.

This choice has had major consequences: the German economy is now paralyzed, and small and medium-sized enterprises are bearing the brunt of the effects. Large companies, particularly chemical companies like BASF, can relocate to India, China, or Vietnam, where costs are lower and regulations less stringent. For SMEs, employees, and subcontractors, this is a disaster.

Although the blame is put largely on dependence on Russian gas in the wake of war in Ukraine, the downward slide was already underway before 2022. Today Russian gas is hardly used for electricity generation in Germany, rather it serves primarily as a raw material for the chemical industry and domestic heating. Germany's electricity problem, it is argued* therefore stems more from flawed political and ideological choices—whose economic consequences are now being felt with brutal force. [µsee e.g: S. Furfari/Atlantico.fr]

ELECTRIC CARS AWITING SHIPPING FOR EXPORT TO EUROPE AT A OVERSEAS PRODUCTION FACILITY

From Development

To Certification

To Trading

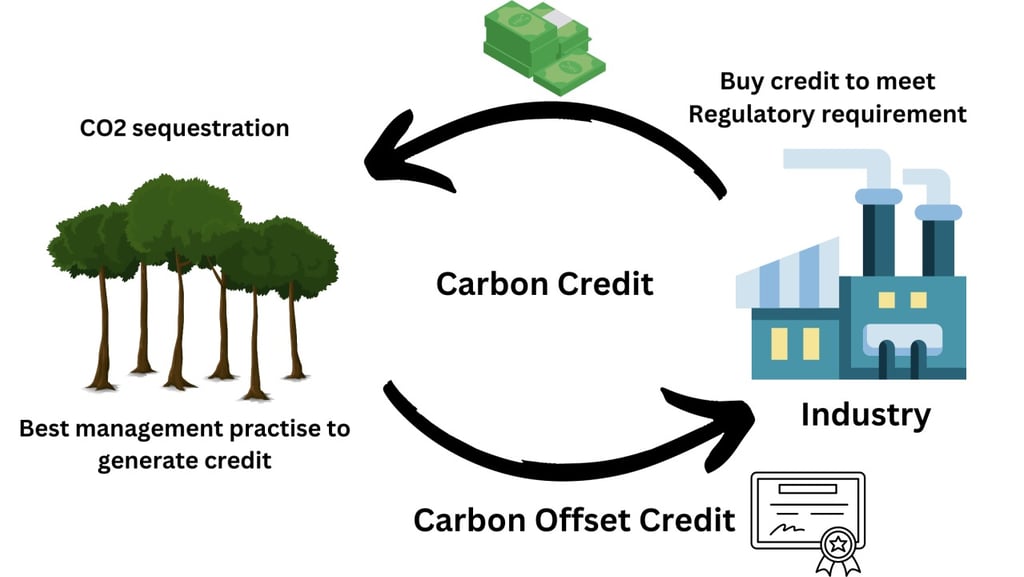

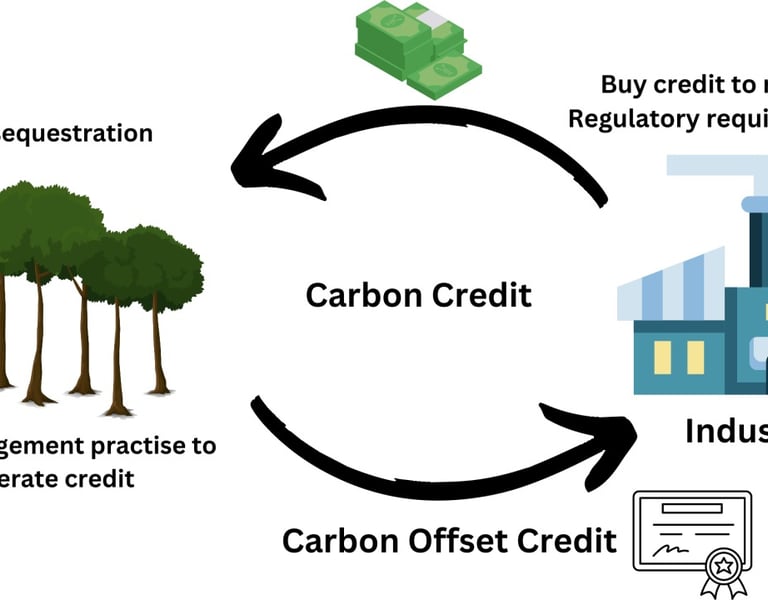

Paths to decarbonisation: Offsets or Credits?

Carbon offsets and carbon credits are closely related concepts in the context of carbon emissions reduction, but they have distinct meanings:

Carbon Offsets

Definition: Carbon offsets are reductions in greenhouse gas emissions (or increases in carbon storage) that can be used to compensate for emissions produced elsewhere. They are typically measured in metric tons of CO2 equivalent.

Function: When a company or individual purchases a carbon offset, they are essentially funding projects (like reforestation, renewable energy, or energy efficiency) that reduce emissions, thereby offsetting their own carbon footprint.

Carbon Credits

Definition: Carbon credits are specific units representing the right to emit one ton of CO2 or its equivalent in other greenhouse gases. They are often created and regulated under cap-and-trade systems.

Function: Companies that reduce their emissions below a certain cap can sell their excess credits to others that exceed their limits. This creates a market for carbon emissions trading.

Regulation: Carbon credits are often part of regulatory frameworks and can be traded in carbon markets, while carbon offsets are generally voluntary and purchased by companies or individuals looking to reduce their impact.

Origin: Carbon credits come from verified emissions reductions tied to regulatory programs, whereas carbon offsets can be generated from a wide variety of projects, which may or may not be verified.

Market Dynamics: Carbon credits are typically subject to market trading and price fluctuations, while carbon offsets are usually sold at a fixed price based on project type and verification.

Key Differences

While both serve to mitigate climate change, carbon credits are more about compliance and regulatory frameworks, while carbon offsets are often voluntary efforts to balance emissions.